Too big to succeed

What happened to GE?

The fall of one of America’s great companies.

GE is a mythic corporation. It was at one time the largest, most powerful company in the world. Its founding story includes the innovator Thomas Edison and financier J.P. Morgan. Its legendary CEO Jack Welch, who wrote five bestselling books on leadership, became a model for an entire generation of executives. When GE started using Microsoft software in our early days, that gave us a huge boost in the market, because GE was such a bellwether company.

It turns out that the word “mythic” is the perfect word for GE. The corporation has come crashing to Earth in one of the greatest downfalls in business history. Its workforce has been hollowed out, from 333,000 employees in 2017 to fewer than 174,000 at the end of last year. Its share price has fallen precipitously. In 2018, GE was dropped from the Dow Jones Industrial Average after more than a century in the index.

GE’s fall is not the result of innovators developing a better jet engine or wind turbine. It’s also not a case of outright fraud, like Enron. It’s a textbook case of mismanagement of an overly complex business.

Only a few people saw it coming (including one, ironically, from J.P. Morgan’s namesake bank). I wish I could tell you that I was one of them, but I was just as surprised as most people.

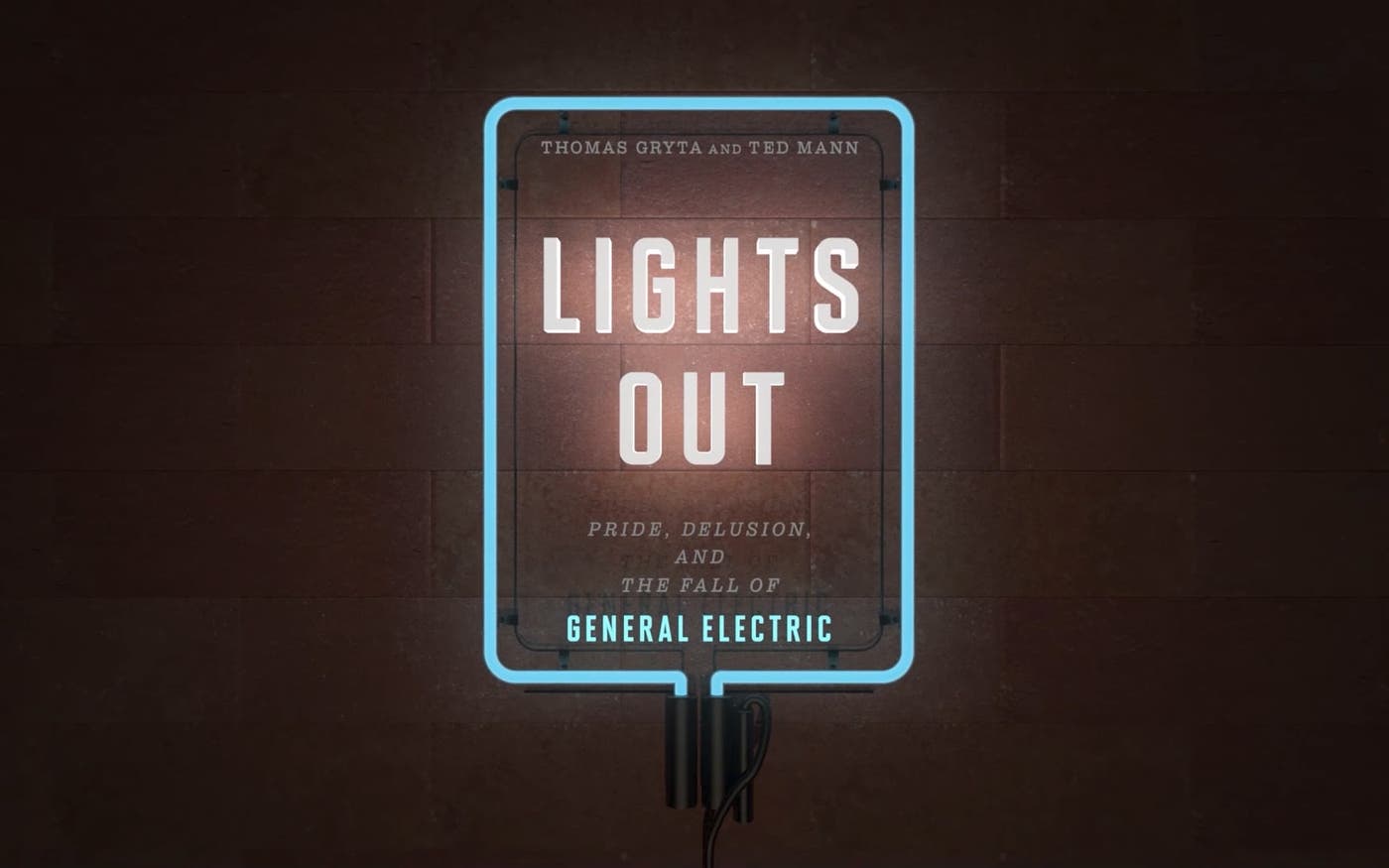

That’s why I was eager to read Lights Out: Pride, Delusion, and the Fall of General Electric, by the Wall Street Journal reporters Thomas Gryta and Ted Mann. I wanted to understand what really went wrong and what lessons this story holds for investors, regulators, business leaders, and business students.

At times, it was a bit hard for me, as a former CEO, to read such harsh criticism of fellow leaders, including people I know and like. But I got a lot out of reading this book. Gryta and Mann gave me the detailed insight I was looking for into the culture, decisions, and accounting that eventually caught up to GE in a gigantic way.

My first big takeaway is that one of GE’s greatest apparent strengths was actually one of its greatest weaknesses. For many years, investors loved GE’s stock because the GE management team always “made their numbers”—that is, the company produced earnings per share at least as large as what Wall Street analysts predicted. It turns out that culture of making the numbers at all costs gave rise to “success theater” and “chasing earnings.” In Gryta and Mann’s words, “Problems [were] hidden for the sake of preserving performance, thus allowing small problems to become big problems before they were detected.”

Chapter 14 of Lights Out details many of the gimmicks GE employed to make the numbers look better than they really were. For example, Gryta and Mann report that GE would sometimes artificially boost quarterly profits by selling an asset (e.g., a diesel train) to a friendly bank, knowing that it could then buy back the asset at a time of GE’s choosing.

There are a lot of ways a company can end up with a culture that rewards gaming the numbers. Although Steve Ballmer and I made our share of strategic mistakes, we were maniacal about making sure our numbers were rock solid and avoiding incentive systems where people could cram a lot of sales into a quarter in order to look good or meet some quota. Satya Nadella works the same way today.

In many companies, bad news travels very slowly, while good news travels fast. We tried hard to combat that. A team member might send me mail saying “we just won a software design competition,” and “isn’t this amazing?” I’d typically respond, “Why am I hearing about this one? That’s not statistically representative. How many competitions did we lose?” I used the term “making bad news travel fast” all the time. I wanted to catch negative trends early, when we could still do something about them.

My second big takeaway from Lights Out is that GE didn’t have the right talent and systems to bundle together a dizzying array of unrelated businesses—including moviemaking, insurance, plastics, and nuclear power plants—and manage them well. Investors bought into the notion that the company’s world-renowned training made it better at managing things than anyone else, and that GE could produce consistent profits even in highly cyclical markets. And GE successfully persuaded people that its generalists could avoid the pitfalls that had tripped up big conglomerates in the past.

In reality, those generalists often didn’t understand the specifics of the industries they had to manage and couldn’t navigate trends in their industries. For example, the authors make the case that CEO Jeff Immelt didn’t have a good handle on its huge banking unit, GE Capital. “Making money from [GE Capital] seemed shockingly simple to him at first, as it had to Welch, but the balance sheets were treacherously complex, and deep risks lurked there and were not always easily spotted in the quarterly profits and losses,” write Gryta and Mann. One former GE executive told the authors that “Immelt struggled with basic concepts—the difference between secured and unsecured debt, for instance, which was fundamental to a lending operation like GE Capital.”

This dynamic was not confined to Immelt. It was rampant throughout the company’s top ranks. As a result, the ability of top executives to understand what was really going on was quite limited. The only people who could actually dig down into the numbers and see what was going on were in finance. And as I mentioned above, the finance people didn’t have much incentive to bring negative news to Welch or Immelt.

In my role at our foundation, I sometimes hear fellow philanthropists say things like, “I just wish my grantees could operate more like a business.” The story of GE, led by very smart men who cared deeply about their work, should tamp down that kind of talk. The truth is that businesses, even the giants of industry, are just as susceptible to mistakes as any nonprofit. Anyone who wants to avoid the mistakes made by GE should read this book.